Time and time again, we see people approaching the purchase of an investment property with the wrong perspective.

The assumption is often made that if a property is negatively geared, you are paying less tax. While correct, you are effectively paying for a tax deduction.

Don’t get me wrong, property can be a great investment vehicle but make sure you have all the facts before taking the plunge into an investment like this.

There are considerable costs when purchasing and servicing a property. True performance in any investment is ultimately measured in “money in VS money out”. Assuming you can service the property from a cash flow perspective, the value in investing in property comes from the long term capital growth. This “buy and hold” approach allows you to ride out the up’s and down’s of the market.

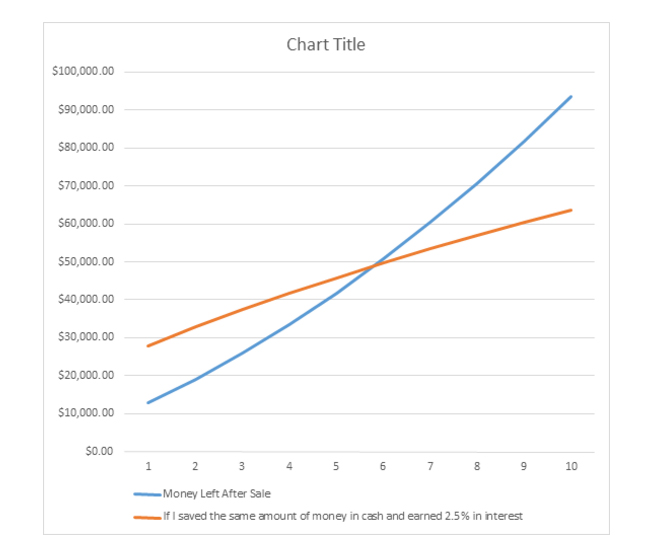

Take for example this theoretical scenario of purchasing a $300,000 property:

- Purchase Price > $300,000.00

- Stamp Duty > $8,500.00

- LMI Paid > $0

- Legals $2,000.00

Cost Base = $308,500.00

- Borrowings > $285,000.00

- Interest Rate > 5.0%

- Capital Gain Percentage > 4.60%

- Average Tax Rate > 20.00%

- Rental Income > $300

The below chart shows break even point at year 6 based on the above figures.

Before looking at property investment, here are some questions you should be asking yourself:

Managing Debt:

- How much can you actually afford and what impact will this have on your personal cash flow?

- How much should I actually borrow? Find the right balance between retaining equity in your current principal place of residence. By putting more money in upfront, you are avoiding lenders mortgage insurance but you then have less deductible debt.

Structuring Debt:

- Is the structure of your debt the most tax efficient setup focused on deductions?

- If something goes wrong such as you lose your job, do you have an exit plan in place to liquidate or finance the asset?

Selecting the Right Property:

- There are so many options from a purchasing perspective. Should you buy a house, duplex or apartment? Do you buy new or established or something that needs some renovating? Each have their pro’s and con’s. Understanding what the implications are from the outset will save heartache and money further down the track.

The unknown factor in all of this is capital growth. While things may be good at the moment, there is always a potential for lacklustre growth. Go in with your eyes open and all the facts to understand how much growth needs to come from your property to ensure it is a good long term investment.

“This document or website contains general advice only. You need to consider with your financial planner, your investment objectives, financial situation and your particular needs prior to making an investment decision. Charter Financial Planning Limited and its authorised representatives do not accept any liability for any errors or omissions of information supplied in this document except for liability under statute which cannot be excluded.”