The March quarter saw one of the worst starts to the calendar year since the global financial crisis (GFC) in 2008. This is in contrast to the very positive end to the 2017 calendar year. And while conditions are not that different to this time last year, with global growth relatively robust, inflation low and government policies still accommodative, a reassessment appears to have occurred in markets.

Optimism was replaced by a more realistic appraisal of what risks and challenges were ahead. And President Trump‘s administration with his comments on trade barriers added to this uncertainty.

Overall moving forward, while economic conditions remain robust, and business confidence is high and corporate earnings continue to rise, tightening financial conditions in the US combined with rising geopolitical uncertainty mean that markets will exhibit higher volatility than experienced last year.

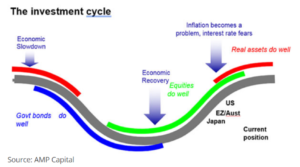

End of the Cycle?

You may have heard the phrase, “we are coming to the end of the cycle”. What they refer to here is the growth of the stock market for the last 10 to 12 years and accommodating (low) interest-rate policy. This cycle is best illustrated by the graphic below.

So, in line with this cycle, when interest rates are starting to rise, due to inflation, particularly in the U.S., we saw in early in 2018, that the U.S. inflation rate was ‘above expectations’. This saw the share market react with large falls.

In addition there is concerns about a trade war.

Trade war?

Donald Trump’s presidential campaign commitment was to “protect” American workers from what he regards as unfair trading practices. While in 2017 his focus was on deregulation and tax reform, which helped share markets, this year his focus is different. The November 2018 U.S. mid-term elections are approaching. Recent Polls show his poor popularity has been pointing to the Republicans losing control of the House, so he is back in campaign mode returning to his campaign commitments on trade, knowing tariffs are popular with his supporters.

But the Tweets he sends out don’t carry over to actual policy. Here are three examples:

- Increase US tariffs on aluminium and steel – Europe has been exempted for now along with most US allies.

- “I may hold it up ….it’s a very strong card” (meaning delay until I want to) the South Korea/U.S. free trade deal (KORUS) – has now been renegotiated with only minor concessions to the U.S. (on steel and cars with a focus on reducing non-tariff trade barriers)

- The free trade Agreement with Mexico and Canada (NAFTA) looks on track to be renegotiated. He originally tweeted he would leave it completely.

On China, reaching a deal with China will be harder than “fixing” KORUS and NAFTA and there is a long way to go with setbacks inevitable, but ultimately a deal is likely.

Australia

Australia remains somewhat out of step with the US-led global growth cycle. Encouragingly, many companies are reporting stronger than anticipated revenue and earnings, and they are delivering higher dividends. However, the overall equity market’s large exposure to interest rate sensitive sectors (infrastructure/utilities/property trusts) continues to inhibit potential share price appreciation.

In addition, the short term outlook for Australian banks remains challenging due to high levels of household debt and an overhang from the Royal Commission into behaviour within the sector.

Sources: Schroder Asset Management/AMP Capital/ipac Investment Management

This document contains information that is general in nature. It does not take into account the objectives, financial situation or needs of any particular person. You need to consider you financial situation and needs before making any decisions based on this information.