Centrelink Changes on January 2017

We have communicated to you earlier regarding these changes and they are now around the corner.

Let’s recap.

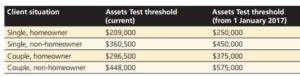

There are two changes to the social security pension Assets Test on 1 January 2017:

- An increase to the Assets Test thresholds (see Table 1), and

- Doubling of the taper rate from $1.50 to $3 per $1,000 of assets per fortnight.

As you can see above, these Assets Test thresholds will allow some clients to hold more assets before their pension starts to reduce under the Assets Test. For some clients with lower asset levels, this may lead to higher pension entitlements.

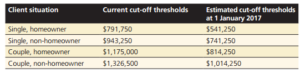

The second change relates to the increase in the taper rate – the rate at which the age pension reduces . This change will reduce Age Pension entitlements at a faster rate once assessable assets exceed the new Assets Test thresholds (Table 2). The largest reduction in pension entitlements will occur at the new Assets Test cut-off thresholds.

For example, as a couple (homeowners), if you are around the $650,000 to $900,000 range of assets, you will either have a significant reduction in the age pension or lose it altogether.

Some clients may simply review and tighten their budgets to offset the reduction (or loss) in their pensions. Others may find this approach challenging, particularly those facing a larger reduction in entitlements. It can also be difficult for clients who are in the early years of retirement, a period when they may be most active. Where clients are looking to maintain their cash flow, there are a number of options and strategies that can help manage the impact of the Assets Test changes.

If you are concerned with the impact these changes will make to your situation, please contact us for a review.

“This document or website contains general advice only. You need to consider with your financial planner, your investment objectives, financial situation and your particular needs prior to making an investment decision. Charter Financial Planning Limited and its authorised representatives do not accept any liability for any errors or omissions of information supplied in this document except for liability under statute which cannot be excluded.”